In 2010, facing the dynamic macro-economic developments and intensified market competition, China Telecom seized the opportunities and leveraged its full services operation to accelerate the development of mobile services and strengthen the integration of the wireline, mobile and Internet services. Mobile services maintained high growth momentum and the risks in wireline services were effectively mitigated. In the meantime, we geared up to grow our 3G services resulting in rapid development in mobile Internet and continuously increasing competitive edges.

In 2010, facing the dynamic macro-economic developments and intensified market competition, China Telecom seized the opportunities and leveraged its full services operation to accelerate the development of mobile services and strengthen the integration of the wireline, mobile and Internet services. Mobile services maintained high growth momentum and the risks in wireline services were effectively mitigated. In the meantime, we geared up to grow our 3G services resulting in rapid development in mobile Internet and continuously increasing competitive edges.

Key Operating Performance

In 2010, the operating revenues were RMB219,864 million. Excluding the amortisation of the upfront connection fees, the operating revenues were RMB219,367 million, grew by 5.4% over last year. The overall business structure of the Company has been further optimised while the revenue from mobile, broadband and other strategic growing services accounted for approximately 50% of the operating revenues.

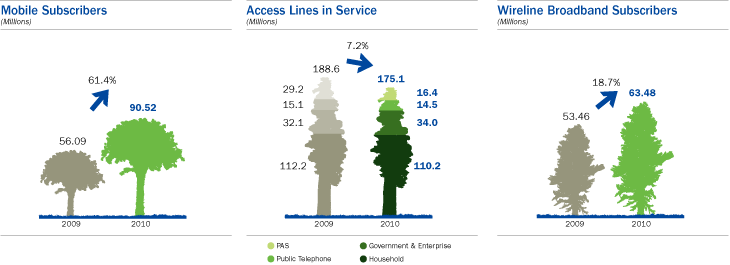

Mobile services maintained high growth momentum in 2010. The Company enhanced its marketing capabilities in target customer groups and actively expanded its mobile subscriber base through the promotion of industry-specific applications, the development of 3G services and the strengthened marketing efforts in key target markets. The number of mobile subscribers reached 90.52 million, 61.4% increase from the beginning of the year. Revenue from mobile services reached RMB47,722 million, an increase of 59.1% over last year, while mobile MOU remained stable.

Mobile services maintained high growth momentum in 2010. The Company enhanced its marketing capabilities in target customer groups and actively expanded its mobile subscriber base through the promotion of industry-specific applications, the development of 3G services and the strengthened marketing efforts in key target markets. The number of mobile subscribers reached 90.52 million, 61.4% increase from the beginning of the year. Revenue from mobile services reached RMB47,722 million, an increase of 59.1% over last year, while mobile MOU remained stable.

Broadband services experienced solid growth in 2010. The Company continued to increase efforts in the development of broadband services, taking advantage of its access network optic fiber upgrade and the trial of the Three Network Convergence. The Company sharpened its competitive edge through bandwidth upgrade and stabilised the value of its broadband services through integrated operation, ensuring the leading position in the market. The total number of wireline broadband subscribers was 63.48 million, an increase of 10.02 million, or 18.7% from last year. Revenue from wireline broadband services was RMB54,127 million, an increase of 15.0% from last year.

Wireline value-added services and integrated information services continued to grow in 2010. We deepened the centralised operations and focused on differentiation of products and services. Best Tone service maintained rapid growth and business-travel applications achieved breakthroughs through the integration of multi-service channels. Revenue from wireline value-added services and integrated information services reached RMB28,312 million, an increase of 1.2% from last year, accounting for 12.9% of the operating revenues excluding amortisation of the upfront connection fees.

Revenue from wireline voice services in 2010 was RMB62,498 million, representing 28.5% of the total operating revenues excluding amortisation of the upfront connection fees. Through deepening of integration, voice traffic promotion based on monthly package and the migration of the PAS subscribers to our mobile services, the decline of wireline subscribers has slowed down, the proportion of PAS subscribers has gradually decreased and hence the risks in wireline services operation have been gradually alleviated.

Business Operating Strategies

In 2010, the Company adhered to its operational philosophy of “innovative differentiation and integration aiming at profitable scale development”, continuing to enhance its capabilities in integrated operation, industry applications promotion, 3G and mobile Internet operation, sales channels optimisation as well as the extension of industry value chain. In particular, the following five business operating strategies have been implemented:

Firstly, we deepened our integrated operation and achieved effective differentiation. The Company promoted in-depth integration of mobile, broadband, wireline voice and integrated information application services. Measures including unified accounts, voice traffic sharing and integration of applications have been taken to boost sales. Focusing on promoting integrated service packages, we tilted our handset subsidy and terminal resources towards mid-to-high-end customers and encouraged low-end users to upgrade to high-end tariff packages. In doing so, we aimed to stablise and increase customer value, enhance customer loyalty, and effectively promote the growth of subscriber base and revenues. As at the end of 2010, the number of mobile subscribers using integrated service packages accounted for 53.0% of the total, a three percentage points increase from the end of 2009. The number of “One Home” subscribers as a percentage of total household subscribers reached 44.0%, 11.6 percentage points increase from the end of 2009. The number of “BizNavigator” subscribers reached 4.99 million, increasing 14.4% from the end of 2009.

Secondly, we focused on the expansion of key industry-specific applications to drive the scale development of mid-to-high-end mobile subscribers. In 2010, we pooled the strength of the Company and focused on the promotion of four key industry-specific applications, namely, government administration and supervision, transportation and logistics, digital hospitals and e-Surfing RFID. These have satisfied customers’ demand for mobile office administration, logistics enquiry, e-hospital registration and telemedicine, and promoted the informatisation in these industries. As a result, industry-specific applications experienced rapid growth month by month, effectively driving the scale development of mid-to-high-end mobile subscribers.

Thirdly, we accelerated 3G development and deployed traffic-centered mobile Internet operation. We optimised 3G service plans to highlight the 3G features of mobile Internet over handsets and mobile value-added services. We tilted subsidies towards 3G development, focusing on the markets of business elites, office staff and young students to develop 3G subscribers with a net increase of 8.22 million subscribers in 2010. We built the 3G key products system, implemented its operation based on product centers and constantly optimised the products. Meanwhile, we cooperated with leading Internet companies to introduce popular Internet applications. The data traffic driven by key 3G products has significantly increased with continuously enhanced application popularity and data traffic value. 3G customers’ value and loyalty are much higher than 2G customers, our data traffic-centric operational strategy achieved initial success.

Fourthly, we optimised the system of distribution channels with increased contribution from open channels in 2010. We made great efforts to promote open channels, taking measures such as penetrating chain stores, introducing dealers into our service halls and direct supply of terminals. Sales through open channels have made breakthroughs in chain stores, the Company’s terminals and services are available for sale in more than 1,000 chain stores of Gome, Suning, FunTalk, and D.PHONE, meeting the target of reaching 2 out of the top 10 local open channels. Mobile terminal sales through open channels exceeded 60% of the total and mobile subscribers registered through open channel reached 50%, indicating increasing importance of open channels in the scale development of mobile services.

Fifthly, driven by the Company’s scale development and tactical guidance, the terminal industry value chain became invigorating. In 2010, the Company promoted the growth of the terminal industry value chain through scale development of mobile subscribers. The Company further standardised terminal supplies and sales mechanism by means of incentive subsidy and factory direct supply. Terminal models proliferated rapidly with continuously enhanced price-performance ratio. During the year, around 45 million CDMA terminals were sold, of which nearly 10 million were EV-DO mobile handsets. The number of 3G terminal models is over 300. Smart phones priced at around RMB1,000 or so such as ZTE N600 and Huawei C8500 and star 3G handset models such as Motorola XT800, Samsung (W799 and i909) were popular in the market. As a result, our mobile terminals achieved further optimised structure with continuously enhanced price-performance ratio, providing more choices to the customers.

Network and Operation Support

In line with the requirement of deepening strategic transformation in 2010, we persisted in tilting investment towards high growth services and high return service regions to enhance return on investment and optimise resource allocation under tight risk control. The Company made major achievements in improving network capacity, strengthening supporting platforms, promoting network evolution and deepening precision management.

In 2010, capital expenditure was RMB43,037 million, an increase of 13.1% from last year. Capital expenditure accounted for 19.6% of operating revenues excluding amortisation of the upfront connection fees, up by 1.3 percentage points from 2009. In order to effectively support the Company’s transformation, we made appropriate modification to investment structure to further increase the weight of investment in broadband and value-added services, which greatly contributed to the scale development of our transformation services. We proactively negotiated with the parent company in mobile network planning to push forward network optimisation and quality enhancement, promoted effective synergy between WiFi and EV-DO and increase network resource utilisation and traffic value. With respect to the bearer network, we speeded up capacity expansion and optimisation of IP, backbone transmission and metropolitan area networks, and actively carried out pilot programs for the next generation network to lay a solid foundation for network and technology evolution.

Regarding the broadband network, we systemically upgraded access networks with optic fiber, and massively deployed Fiber-To-The-Home (FTTH), achieving significant enhancement of customer access bandwidth. In 2010, investment in broadband and Internet services was RMB27,630 million, accounting for 64.2% of the total capital expenditure, up by 10.1 percentage points from last year. By the end of 2010, broadband access capacity increased by 17.90 million ports over the year; the 20M and 4M bandwidth coverage in urban areas (including the counties) were 58% and 98% respectively, representing an increase of 22 and 3 percentage points from the end of 2009, respectively. Meanwhile, in order to give a full play of WiFi networks as the extension and supplement to wireline broadband and 3G networks, with a view to diverting data traffic from EV-DO to WiFi, we continued to increase our investment in WiFi networks. By the end of 2010, the number of WiFi hotspots reached 100,000.

Regarding the broadband network, we systemically upgraded access networks with optic fiber, and massively deployed Fiber-To-The-Home (FTTH), achieving significant enhancement of customer access bandwidth. In 2010, investment in broadband and Internet services was RMB27,630 million, accounting for 64.2% of the total capital expenditure, up by 10.1 percentage points from last year. By the end of 2010, broadband access capacity increased by 17.90 million ports over the year; the 20M and 4M bandwidth coverage in urban areas (including the counties) were 58% and 98% respectively, representing an increase of 22 and 3 percentage points from the end of 2009, respectively. Meanwhile, in order to give a full play of WiFi networks as the extension and supplement to wireline broadband and 3G networks, with a view to diverting data traffic from EV-DO to WiFi, we continued to increase our investment in WiFi networks. By the end of 2010, the number of WiFi hotspots reached 100,000.

Operating Highlights in 2011

In 2011, in order to grasp growth opportunities in the fast evolving mobile Internet market and tackle the challenges brought by fierce competition in current and emerging business, the Company will continue to stick to its “Customer-Focused Innovative Informatisation” strategy. Positioning itself as “a leader of intelligent pipeline, a provider of integrated platforms, and a participant of content and application development”, the Company will promote scale growth of subscriber base in full swing. We will further deepen integrated development and continuously optimise business structure, progressively transforming to a mobile Internet operating mode. In particular, we will build differentiated edges with increasing focus on 3G services and continuously enhance scale development of industry applications to promote the expansion of mid-to-high-end government and enterprise customers. We will push forward broadband speed upgrade to keep our competitive edges. We will take measures to further alleviate the risk of wireline voice services to promote harmonious full services operation. Meanwhile, we will continue to strengthen network optimisation, operation and maintenance, aiming at enhancing service capacity for full services operation and forging innovative and differentiated competitive edge.